Why So Many Elkhart TX Homeowners Lose Money On Roof Insurance Claims

Our town sees its fair share of hail, high winds, and surprise thunderstorms, and we have noticed the same painful pattern over and over: homeowners think their roof is “mostly fine,” file an insurance claim on their own, and end up leaving thousands of dollars on the table. They often only discover the problem years later, when leaks appear and repairs are suddenly all out-of-pocket. By then, it’s too late to reopen the claim or recoup what was lost.

From what we have seen in Elkhart TX, the biggest issue is not that insurance companies are evil or that adjusters are dishonest. The real problem is that the process is stacked in favor of the carrier’s expertise, not the homeowner’s. The company has pros—adjusters, estimators, engineers—working every angle of the policy. Most families are doing this for the first time and just assume the initial offer is “what they’re owed.” That’s where money quietly slips away.

We have made it our mission to help neighbors understand what’s really happening during a roof damage insurance claim. When we walk homeowners through a storm inspection, policy review, and the scope of repairs, we almost always find missed items. It may be a few missing line items on the estimate, or it might be an entire section of the roof or guttering that never made it into the report at all. Either way, the impact is the same: less money to restore the property to pre-storm condition.

In Elkhart TX, roofs are more than just shingles. We have flashing, vents, boots, decking, ridge caps, and ventilation systems that all need to function together to protect the home. If some of those components are damaged but never documented, the payout won’t cover a full, code-compliant repair. Our passion is making sure local homeowners don’t accept a bare-minimum patch when their policy is supposed to pay for a complete, high-quality restoration.

The Hidden Ways Roof Damage Gets Overlooked In Elkhart TX

Our team has inspected hundreds of roofs after storms in East Texas, and we see the same types of missed or underestimated damage appearing on insurance claim reports. Most of this is not obvious from the ground, and it’s easy for a rushed or inexperienced adjuster to gloss over it. When that happens, the damage keeps getting worse while the homeowner assumes everything was handled correctly.

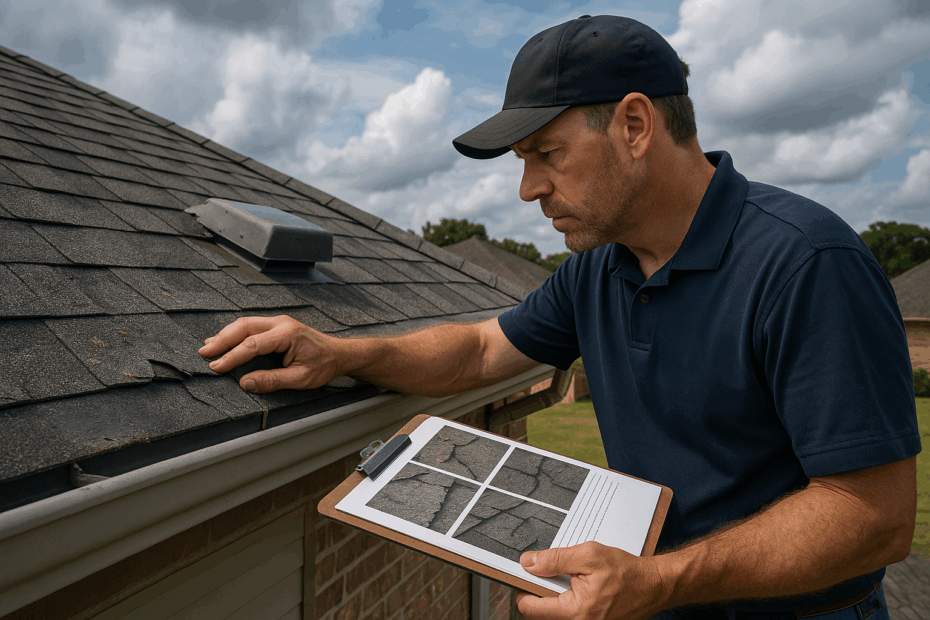

Subtle Shingle Damage That Looks “Normal” From The Yard

We have often climbed onto roofs in Elkhart TX that were “cleared” by an adjuster, only to find clear evidence of storm damage. From the driveway, the roof may look acceptable. Up close, it’s a different story.

Some of the hidden problems we routinely find include:

– Hail bruises: Granules knocked off the shingle surface, exposing the asphalt. These spots shorten the shingle’s lifespan and can lead to leaks over time.

– Cracked or fractured shingles: Wind can bend shingles back, causing hairline cracks that are almost impossible to see from the yard.

– Lifted or unsealed shingles: Shingles that were peeled up by wind may reseal poorly or not at all. They can blow off with the next storm.

– Damaged ridge caps: Ridge shingles take the brunt of wind and hail. If they’re not properly included in the inspection and estimate, the roof’s most vulnerable point remains compromised.

Our experience has shown that even one square of heavily damaged shingles in the right location can justify a broader replacement under many policies. But if that’s never documented correctly during the insurance claim, the carrier will only pay for cosmetic patches, not a long-term solution.

The “Non-Roof” Items That Should Still Be Part Of Your Claim

A roof storm event rarely damages only shingles. We have seen:

– Bent or cracked gutters

– Dented fascia metal

– Damaged downspouts and gutter guards

– Broken turbine vents or ridge vents

– Chipped paint and trim around the eaves

– Screens and window beading damaged by hail

These might seem minor, but they all add up. When a complete, accurate inspection is done, the total scope of the job grows—and so does the check that helps restore your home. Many homeowners in Elkhart TX never realize that these components should be addressed in the same insurance claim as the roof.

If a roof contractor doesn’t walk the entire exterior, check for collateral damage, and review code requirements, those line items never make it into the estimate. We prefer to create a thorough, photo-documented report that shows the full story of what the storm did to your property. That way, the adjuster has clear evidence to approve the necessary repairs, not just guesses or verbal descriptions.

How Insurance Claim Policies Really Work (And Why It Matters In Elkhart TX)

We have learned that the biggest gap in the process is not hail size or wind speed—it’s understanding. Most people don’t really know how their roof coverage works until they’re already in a stressful situation. By then, deadlines are ticking, calls with the carrier are rushed, and important decisions are made without the right information. That’s when small mistakes can lead to big financial losses.

Actual Cash Value vs. Replacement Cost Value

At the heart of almost every roof insurance claim is the question of how the payout is calculated. Two key terms matter a lot:

– Actual Cash Value (ACV): This is the depreciated value of your roof. The carrier takes the replacement cost and subtracts an amount for age and wear. You receive a smaller check up front.

– Replacement Cost Value (RCV): This is the full cost to replace the roof at today’s prices, if you meet the policy conditions and complete the work.

Many Elkhart TX homeowners have replacement cost policies but only ever collect the ACV portion because they don’t complete the documented repairs under the claim, or they don’t submit final invoices and photos. We have seen situations where thousands of dollars in “recoverable depreciation” never gets released simply because the paperwork wasn’t finished properly.

Our approach is to walk homeowners through the entire process:

1. Verify whether the policy is ACV or RCV.

2. Confirm what’s required to unlock the full RCV funds.

3. Make sure the final invoice and documents match the agreed scope of work.

4. Help provide completion photos when needed to finalize the claim.

When we do this, the final payout in Elkhart TX is often significantly higher than what the homeowner thought was possible when they first opened the claim.

Deductibles, Exclusions, And Coverage Gaps

Another area where money is lost is misunderstanding deductibles and exclusions. Our town has plenty of older homes, metal roofs, and mixed-material roofs, and each of these can affect what the carrier will pay.

Common issues we see include:

– High wind/hail deductibles: Some policies have separate, higher deductibles for roof-related events. Homeowners are surprised when their out-of-pocket portion is much larger.

– Cosmetic-only exclusions: Certain policies limit coverage on metal roofs to “functional” damage only, not cosmetic dings or dents.

– Age-based exclusions: Older roofs may have reduced coverage or special conditions attached.

We believe it’s critical to read the policy, not just skim the declarations page. When we assist with an insurance claim in Elkhart TX, we always encourage homeowners to ask:

– What is my named storm or wind/hail deductible?

– Do I have Actual Cash Value or Replacement Cost coverage on the roof?

– Are there any cosmetic damage exclusions?

– Are code upgrades covered if my roof has to be brought up to current standards?

Understanding these details ahead of time can help you set realistic expectations, choose the right contractor strategy, and avoid nasty surprises after the adjuster’s visit.

The Costly Mistakes Homeowners Make During A Roof Insurance Claim

We have watched neighbors in Elkhart TX make the same well-intentioned missteps over and over during the claims process. None of these come from a place of carelessness; they come from trusting that “the system” will take care of them. Unfortunately, that’s not how it usually works. Avoiding a few key mistakes can preserve thousands of dollars in coverage that would otherwise slip away.

Trusting A Quick Visual Check Instead Of A Professional Inspection

A common pattern we see is:

– A storm hits.

– An adjuster comes out and spends 10–20 minutes on the roof.

– The homeowner watches from the driveway and sees no obvious panic.

– A short time later, they get a small check or a “no damage” letter.

This process might sound normal, but it’s not always thorough. Our inspections usually take longer, involve detailed photos, and include measurements for every slope, valley, ridge, and accessory. We also check:

– Attic spaces for hidden leaks or water staining

– Ventilation and intake/exhaust balance

– Decking condition under soft or spongy spots

– Nearby fences, AC units, and siding for storm impact clues

When we compare our findings to an initial adjuster report, we often see missing items. Those items represent real dollars—funds that should be available to restore the home. Without a contractor’s detailed documentation, they never get added to the claim.

Not Challenging An Incomplete Or Underpaid Estimate

We have found that many homeowners think the adjuster’s estimate is final and non-negotiable. In reality, if new evidence, code requirements, or missed damage are brought to light, the carrier can—and often does—revisit the estimate.

Here’s what we often help with in Elkhart TX:

– Supplementing the claim with additional photos and measurements

– Providing manufacturer documentation that shows why certain materials or methods are required

– Citing local building codes that require upgraded underlayment, ventilation, or flashing details

– Requesting a reinspection when appropriate

By approaching this professionally and respectfully, we’ve seen significant increases in approved claim amounts. We don’t view it as “fighting” the insurance company; we see it as making sure the full, legitimate scope of work is recognized and funded.

Choosing The Lowest Bid Instead Of The Right Scope

Another costly mistake is accepting a contractor simply because they promise to “do the job for the insurance amount” or beat everyone’s price. We have seen this lead to:

– Cheaper, lower-quality materials substituted for what the policy is actually paying for

– Skipped steps like proper underlayment, starter strips, or ice and water shield in critical areas

– No documentation of the finished work, which can make it harder to release recoverable depreciation

Instead of asking, “Who can do it cheapest?” we encourage homeowners in Elkhart TX to ask:

– Who will match the scope of work to the approved estimate?

– Who understands local code and manufacturer requirements?

– Who will help document the work for the final claim payment?

– Who will be here years from now if there’s a workmanship issue?

Our goal is always to install a roof that truly restores the property to its pre-loss condition, not just cover it with new shingles. When that’s done correctly, the numbers in the insurance claim and the quality of the finished work line up the way they should.

A Step-By-Step Approach To Protect Your Roof Investment In Elkhart TX

Over the years, we have developed a clear, repeatable process to help our neighbors handle a roof insurance claim without leaving money behind. It’s not complicated, but it does require taking things in the right order, rather than rushing straight to a phone call with the carrier.

Step 1: Get A Professional, Local Inspection Before You File

We always recommend that homeowners in Elkhart TX call a trusted local roofing company before calling the insurance company. Here’s why:

– We can confirm whether storm damage is present and significant enough to justify a claim.

– We can document damage thoroughly with photos and notes, creating a strong foundation for the claim.

– We can identify pre-existing issues that might complicate the process, such as old leaks or prior repairs.

During our inspection process, we typically:

– Walk every slope of the roof

– Check flashings, pipe boots, vents, and valleys

– Inspect gutters, fascia, and exterior trim

– Look inside the attic for evidence of water intrusion

If the damage is minimal and doesn’t justify a claim, we’ll say so. If it does warrant a claim, we’ll help you prepare for the adjuster visit so you know what to expect.

Step 2: Open The Insurance Claim Strategically

Once we see clear storm-related damage, it’s time to open the claim. We encourage Elkhart TX homeowners to:

– Have their policy information handy

– Take notes on who they speak with and any claim numbers provided

– Ask what the next steps are and when to expect an adjuster visit

We can’t file the claim for you, but we can stand with you as a knowledgeable ally, helping you understand the language and expectations. Our presence during the adjuster’s visit ensures that all damage is pointed out and nothing is unintentionally overlooked.

Step 3: Review, Supplement, And Approve The Scope Of Work

Once the adjuster’s estimate is complete, we compare it to our own findings. If everything matches, great—we move forward. If there are missing items, code-required components, or pricing discrepancies, we help prepare supplemental documentation.

This can include:

– Detailed photo reports

– Material lists and cost breakdowns

– Manufacturer installation requirements

– Local building code references

Our aim is not to inflate the claim, but to ensure it is accurate and sufficient to do the job correctly. When the scope is agreed upon, we sit down with the homeowner to review materials, colors, scheduling, and any upgrade options they may want to add out-of-pocket.

Step 4: Complete The Work And Secure Final Payment

After the roof replacement or repair is complete, we provide:

– Final invoices that match the approved scope

– Completion photos for the insurance company if requested

– Warranty information for both materials and workmanship

The carrier will typically release any remaining recoverable depreciation once they see proof that the work has been completed. We make sure the homeowner understands how this process works and what to expect as the claim closes out. In Elkhart TX, this final step is where many people unintentionally lose money—by failing to submit needed documentation or waiting too long to finalize their claim. We help prevent that.

Protecting Your Home, Your Wallet, And Your Peace Of Mind

We have seen too many families in Elkhart TX discover, months or even years later, that their roof insurance claim didn’t truly cover what it should have. By then, leaks have developed, wood has rotted, and out-of-pocket repair costs feel like an unfair second hit after the storm itself. It doesn’t have to be that way.

The key is to slow down, get informed, and surround yourself with the right support:

– A thorough, honest inspection from a local roofer who understands storm damage

– A clear understanding of your policy, including deductibles and whether you have ACV or RCV coverage

– A complete, documented scope of work that meets local codes and manufacturer requirements

– A willingness to challenge incomplete estimates through professional supplements when necessary

When these pieces are in place, an insurance claim becomes what it was meant to be: a tool to restore your home, not a guessing game that leaves you short. Our passion is helping homeowners navigate that process with confidence, so they don’t unknowingly lose money on one of their most important assets.

If you live in Elkhart TX and suspect your roof has been damaged by hail, wind, or a recent storm, we invite you to reach out to us for a detailed inspection and claim guidance. You can learn more about our services and request an appointment at https://reliableroofingeasttexas.com/. We are here to help you protect your home, your budget, and your peace of mind—one roof at a time.